Deeper in Debt: For-Profit Schools Driving Student Loan Default in New York State

Nearly a quarter of undergraduate students in New York State who take out student loans either default or are at high risk of default after five years, driven by disproportionately high default rates at the state’s for-profit schools. The data underscores the need to tackle the student debt crisis in New York and suggests that state policymakers should take steps to hold the most default-prone institutions accountable.

by Eli Dvorkin, Jonathan Bowles, and Charles Shaviro

Nearly a quarter of undergraduate students in New York State who take out student loans default or are at high risk of default after five years, according to our new analysis of five-year data loan outcomes for students at 240 higher education institutions across the state. While New York’s overall five-year default rate of 11 percent is below the national average of 15 percent, it is cause for serious concern when more than 1-in-10 student borrowers are defaulting. Another 13 percent of borrowers were at high risk of default after five years.

This data brief—the first comprehensive analysis of five-year student loan outcomes in New York—reveals that the student loan default rate in New York is higher than many previously believed. Indeed, previous research focused only on the default rate three years after students took out a loan. Our analysis shows student loan default rates in New York nearly double between the third and fifth year—from 6.5 percent to 11 percent.

We also find that the state’s for-profit higher education institutions are responsible for a disproportionate share of all student loan defaults after five years, with students attending for-profit schools defaulting at more than double the rate of public colleges.

Taken together, the data underscores the need to tackle the student debt crisis in New York and suggests that state policymakers should take steps to hold the most default-prone institutions accountable.

Addressing this problem will only become more important as the value of a college credential continues to rise across New York State. In fast-growing occupations like marketing and software development and in sectors from healthcare to education, a well-paying job increasingly requires some form of postsecondary credential, and most income gains have accrued to workers with at least a bachelor’s degree. But while so many striving New Yorkers feel the pressure to pursue an education at any cost, too many of these students are seeing their dreams of a middle-class life derailed by debilitating debt.

The data shows that outcomes at the state’s for-profit higher education institutions are particular cause for concern. Although just 6 percent of all undergraduate students in New York attended for-profit schools during the period of our analysis, these schools accounted for 41 percent of all student loan defaults after five years. There continue to be a number of reputable for-profit institutions across the state that provide significant value to student. However, more students at for-profit schools defaulted after five years than did public college students—even though public colleges in New York enroll almost ten times as many students as for-profit institutions.

This report analyzes data from the U.S. Department of Education on the outcomes of New York's federal student loan borrowers who entered repayment in 2012, covering the period from 2012 to 2016.

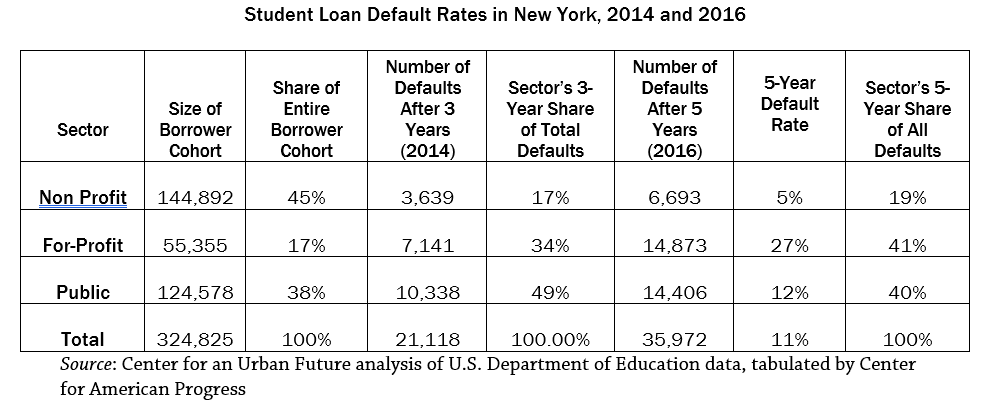

Between 2014 and 2016, the number of New York student loan borrowers in default rose from 21,118 (6.5 percent of all borrowers) to 35,972, (11 percent). Another 13 percent of borrowers were at high risk of default after five years.

In total, nearly one-quarter (24 percent) of New York’s student loan borrowers were facing serious financial struggles to repay or had already defaulted after five years.

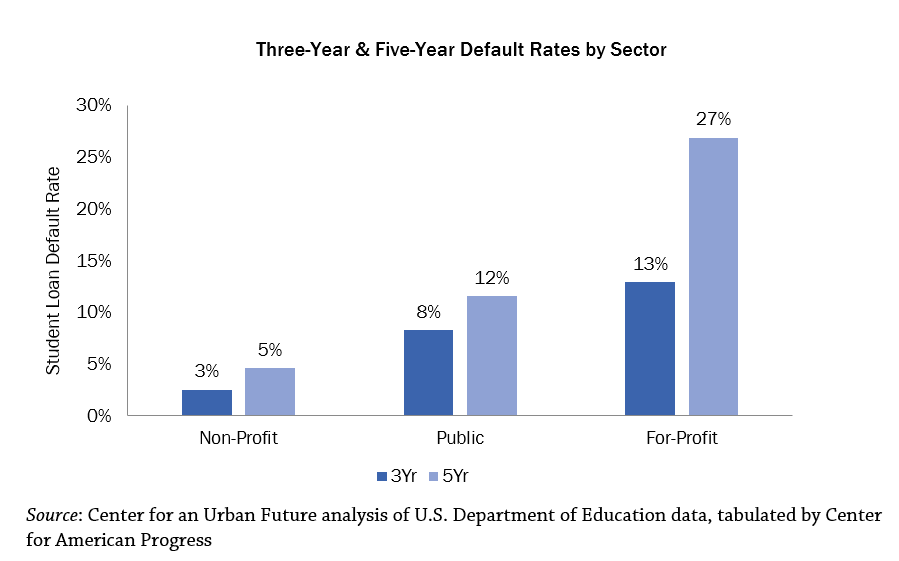

The for-profit higher education sector is driving student loan defaults in New York. After five years, 27 percent of student loan borrowers who attended for-profit institutions defaulted, compared to 12 percent of students who attended SUNY or CUNY colleges and 5 percent of students who attended private non-profit colleges.1

The for-profit higher education sector accounts for 6 percent of all undergraduate students in New York and 17 percent of student loan borrowers—but 41 percent of borrowers who defaulted after five years. More for-profit students defaulted after five years than public college students, even though public colleges in New York enroll almost ten times as many students as for-profit institutions.

Twenty-one New York State higher education institutions had a five-year default rate of 30 percent or higher. All were for-profit institutions. Thirteen of the 21 high-default-rate schools subsequently shut down.

Of the 21 schools with a five-year default rate of 30 percent or higher, six were Manhattan, four in Queens (4) and four on Long Island. The other “high-default-rate” schools were in Albany (1), Binghamton (1), Buffalo (1), Elmira (1), Liverpool (1), Oswego (1), and Rochester (1).

Of the 72 schools with a five-year default rate of 20 percent or higher, 11 were in Manhattan, 10 in Queens, and 9 on Long Island. The other locations with the most institutions with at least a 20 percent default rate were: Albany (with four schools), Rochester (4), Brooklyn (2), Buffalo (2), Elmira (2), Liverpool (2), Schenectady (2), Utica (2), West Seneca (2), and White Plains (2).

New York’s five-year student loan default rate of 11 percent is below the national average of 15 percent. Default rates for nonprofit and public institutions were lower (5 percent and 12 percent in New York, versus 9 percent and 14 percent nationally), while for-profit default rates were even higher (27 percent in New York, versus 25 percent nationally).

After three years, just one of New York’s higher education institutions had a default rate above the U.S. Department of Education’s threshold for losing access to financial aid. After five years, 21 schools (6 percent) exceeded the limit.

In the fifth year, 21 schools have default rates at 30 percent or higher. Three schools have default rates over 40 percent, and one of those schools has a default rate over 50 percent.

All of the “high-default-rate” institutions in the state are for-profit schools. Seven mainly offer associate degrees, while the other 14 mainly offer certificates. The largest institution is Bryant & Stratton-Buffalo (30 percent). The school with the highest five-year default rate is New Life Business Institute (51 percent), which is not a degree-granting institution.

Thirteen of the 21 high-default-rate institutions subsequently closed, suggesting that five-year default rates above 30 percent may serve as a leading indicator for other issues of concern. In addition, the closure of the schools may have worsened default rates by reducing the credibility of their credentials and eliminating career services support.

At Year Five, 36 institutions have default rates below 5 percent, led by Cornell University with a five-year default rate of 1.1 percent. Of these low-default institutions, 26 were private non-profit schools and the other 10 were public schools.

Only two for-profit institutions had a five-year default rate below 10 percent: the School for Visual Arts (6 percent) and the Institute for Culinary Education (8 percent).

This new data brief by the Center for an Urban Future builds on a thought-provoking 2018 report by the Center for American Progress (CAP), which analyzed new data from the U.S. Department of Education to examine five-year default rates for students nationwide.2 We used CAP’s student loan default database to examine the five-year student loan outcomes of students in New York.3

Other key findings of our New York analysis include:

Student loan defaults rose sharply between 2014 (Year Three) and 2016 (Year Five).

In 2011, 324,825 students entered repayment in New York.

After three years, 6.5 percent of New York student loan borrowers (21,118) had defaulted. After five years, 11 percent of borrowers (35,972) had defaulted.

After three years, only one institution (0.3 percent of all schools in the sample) had a default rate over 30 percent, the threshold at which a higher education institution can lose eligibility to receive federal grants and loans. After five years, 21 institutions (6 percent) had a default rate of 30 percent or higher.

The New York rate of student loan default (11 percent) was lower than the national rate of 15 percent. The share of schools with a high default rate (6 percent) was also lower than the national rate of 13 percent.

For-profit higher education institutions play a disproportionate role in student loan defaults, especially after Year Three.

Only a small fraction of New York’s undergraduate students attend for-profit institutions: as of 2017, the for-profit sector enrolled 59,540 undergraduate students, 6 percent of all New York students.

For-profit institutions play a much larger role in borrowing and default. One in six student loan borrowers (17 percent) attended a for-profit school. After three years, one in three defaulters (34 percent) were former for-profit students. After five years, 41 percent of student loan defaulters were former for-profit students. Only 40 percent of defaulters had attended a public college, even though CUNY and SUNY collectively enroll 58 percent of all undergraduate students in New York.

Between Year Three and Year Five, more than half (52 percent) of the 14,854 New York students who defaulted were former for-profit students, more defaulters than at all public colleges combined.

At Year Five, an additional 19 percent of student loan borrowers from the for-profit sector were at risk of default, compared to 13 percent of students from the public sector and 10 percent of students from the private non-profit sector.

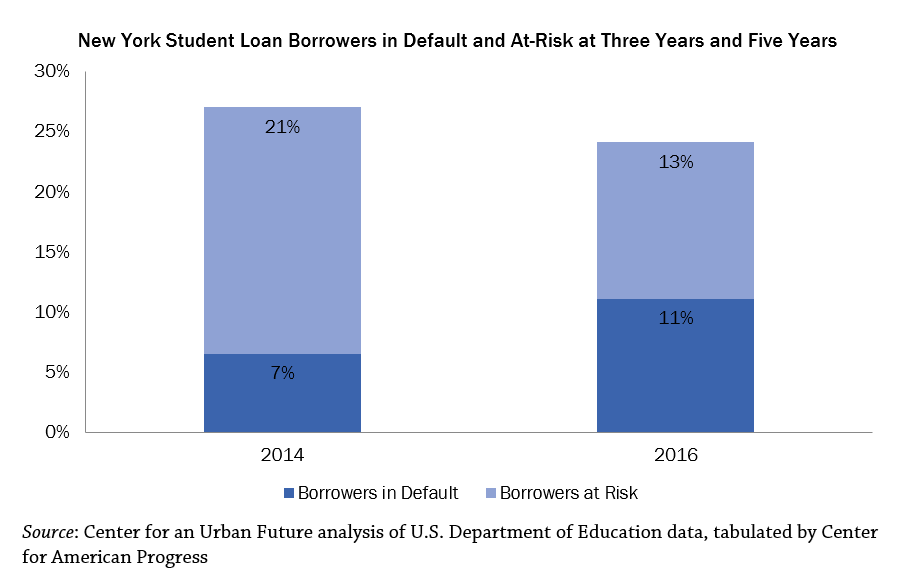

The number of at-risk borrowers declined as defaults rose.

In Year Three, 20.5 percent of borrowers were at risk of default. By Year Five, the number of at-risk borrowers dropped to 13 percent as the number in default rose.

In Year Three, 27 percent of all student loan borrowers were either in default or at risk of default. As of Year Five, 24 percent of borrowers were in default or at-risk.

Individual institutions with high and low default rates vary by ownership sector.

At Year Five, 21 institutions have default rates at 30 percent or higher. Three schools have default rates over 40 percent, and one of those schools has a default rate over 50 percent.

All “high-default-rate” schools are for-profit institutions. Seven mainly offer associate degrees, while the other 14 mainly offer certificates. The largest college is Bryant & Stratton-Buffalo (30 percent). The institution with the highest five-year default rate is New Life Business Institute (51 percent).

Thirteen of the 21 high-default-rate schools subsequently closed, suggesting that five-year default rates above 30 percent may serve as a leading indicator for other issues of concern. In addition, the closure of the schools may have worsened default rates by reducing the credibility of their credentials and eliminating career services support.

At Year Five, 36 institutions have default rates below 5 percent, led by Cornell University with a five-year default rate of 1.1 percent. Of these low-default colleges, 26 were private non-profit institutions and the other 10 were public colleges.

Only two for-profit institutions had a five-year default rate below 10 percent: the School of Visual Arts (6 percent) and the Institute for Culinary Education (8 percent).

New York State Institutions With Five-Year Student Loan Default Rate Above 30 Percent

Institution

Main Credential

Location

Cohort Size

5-Yr Default Rate

Closed?

New Life Business Institute

For-Profit <2-Year

Jamaica, NY

234

51%

Yes

Berk Trade and Business School

For-Profit <2-Year

Long Island City, NY

146

45%

No

Apex Technical School

For-Profit <2-Year

Long Island City, NY

1,599

44%

No

Career Institute of Health and Technology

For-Profit <2-Year

Garden City, NY

721

39%

Yes

Everest Institute-Rochester

For-Profit Associate

Rochester, NY

1,394

37%

Yes

New York Automotive and Diesel Institute

For-Profit <2-Year

Jamaica, NY

328

37%

No

Suburban Technical School

For-Profit <2-Year

Hempstead, NY

461

37%

Yes

Phillips Hairstyling Institute

For-Profit <2-Year

Oswego, NY

78

35%

Yes

Technical Career Institutes

For-Profit Associate

New York, NY

3,300

34%

Yes

Micropower Career Institute

For-Profit <2-Year

New York, NY

248

34%

Yes

Ridley-Lowell Business & Technical Institute-Binghamton

For-Profit <2-Year

Binghamton, NY

171

33%

No

Star Career Academy-New York

For-Profit <2-Year

New York, NY

1,390

32%

Yes

SBI Campus-An Affiliate of Sanford-Brown

For-Profit Associate

Melville, NY

1,011

32%

Yes

Culinary Academy of Long Island

For-Profit <2-Year

Syosset, NY

1,868

32%

Yes

Globe Institute of Technology

For-Profit Associate

New York, NY

176

31%

Yes

Elmira Business Institute

For-Profit Associate

Elmira, NY

433

31%

Yes

SAE Institute of Technology-New York

For-Profit <2-Year

New York, NY

134

31%

No

Bryant & Stratton College-Buffalo

For-Profit Associate

Buffalo, NY

10,856

30%

No

New School of Radio and Television

For-Profit <2-Year

Albany, NY

69

30%

No

The Art Institute of New York City

For-Profit Associate

New York, NY

1,028

30%

Yes

National Tractor Trailer School Inc-Liverpool

For-Profit <2-Year

Liverpool, NY

503

30%

No

Total

26,148

35%

Source: Center for an Urban Future analysis of U.S. Department of Education data, tabulated by Center for American Progress.

To address the student loan default crisis head-on, Governor Cuomo and the State Legislature will need to ensure that default-prone higher education institutions are held accountable and to direct tuition assistance dollars toward colleges that are better serving students. The first step is to identify colleges that rely on potentially unsustainable student debt, such as colleges at which more than half of students take out loans and graduates typically earn wages at or below the level of high school graduates. After identifying these colleges, the state should impose a heightened level of oversight, with mandatory state accreditation, a factual review of marketing and recruitment materials and practices, and conditions on eligibility for state Tuition Assistance Program grants, where applicable. However, many of the state's higher education institutions with the highest student default rates are not eligible for TAP funding, so policymakers should look at other mechanisms to hold institutions accountable, including the oversight authority of the State Department of Education's Bureau of Proprietary School Supervision and the State Division of Veterans' Affairs, which oversees education and training through G.I. Bill benefits. These safeguards can protect the interests of New York’s students and taxpayers, while helping to incentivize better outcomes.

Methodology

The U.S. Department of Education shared data on student loan defaults and repayment activity from 2012 to 2016 with the Center for American Progress, which in turn posted the dataset online. The Center for an Urban Future extracted data on New York State for additional analysis. The data includes outcomes of all federal student loans that entered repayment in 2012 (that is, when the student left the higher education institution and became responsible for regular student loan payments), aggregated at the campus level. Year Three is used by the U.S. Department of Education to determine the Cohort Default Rate (CDR) and assess college eligibility to receive federal financial aid. Borrowers at risk of default (“at-risk borrowers”) are defined as borrowers who are either more than 90 days delinquent on their loans or have not made any payments for reasons other than going back to school or serving in the military. The database includes 240 higher education institutions with default information, excluding another 88 schgols that did not report on student loan defaults.

Endnotes

1. A small percentage of students also attend BOCES continuing education institutions, which are operated by consortia of local school districts.

General operating support for the Center for an Urban Future has been provided by The Clark Foundation, the Bernard F. and Alva B. Gimbel Foundation, and the Altman Foundation. Additional support provided by the Working Poor Families Project, a national initiative supported by the Annie E. Casey and Joyce Foundations, which partners with nonprofit organizations in 23 states to investigate policies that could better prepare working families for a more secure economic future. CUF is also grateful for support from Fisher Brothers and Winston C. Fisher for the Middle Class Jobs Project.

"Deeper in Debt: For-Profit Schools Driving Student Loan Default in New York State" is a publication of the Center for an Urban Future. Researched and written by Eli Dvorkin and Jonathan Bowles. Data analysis by Charles Shaviro. Special thanks to former CUF Senior Fellow for Economic Opportunity Tom Hilliard for initiating this publication.

Center for an Urban Future (CUF) is an independent, nonprofit think tank that generates innovative policies to create jobs, reduce inequality and help lower income New Yorkers climb into the middle class. For 20 years, CUF has published accessible, data-driven reports on ways to grow and diversify the economy and expand opportunity that are anchored in rigorous research, not preconceived notions about outcome. Our work has been a powerful catalyst for policy change in New York City and serves as an invaluable resource for government officials, community groups, nonprofit practitioners and business leaders as they advocate for and implement policies to address some of New York’s biggest challenges and opportunities.

General operating support for the Center for an Urban Future has been provided by The Clark Foundation, the Bernard F. and Alva B. Gimbel Foundation, and the Altman Foundation. Additional support provided by the Working Poor Families Project, and from Fisher Brothers for the Middle Class Jobs Project.